My love of Berkshire Hathaway is rather well documented. It is one of the cornerstones of the Biznews Global Share portfolio and am such a big fan that I even wrote a book about the investment secrets of its chairman Warren Buffett. His AGM is scheduled for next weekend and as it will be webcast for the first time ever, we don’t need to make the 26 hour trip from Joburg to Omaha to take in the five and a half hours of Buffett (and Charlie Munger) wisdom. Here’s a bit of preparation ahead of the AGM from another fan – Cadiz’s Razeen Dinath who explains why Berkshire is a great investment right now. Who am I to disagree? – Alec Hogg

By Razeen Dinath*

Berkshire Hathaway, which is run by well-known investors Warren Buffett and Charlie Munger, has consistently outperformed the S&P 500 Index for three decades. In this article, Razeen Dinath explains why we are optimistic about our significant holding in Berkshire Hathaway by measuring the company against our investment criteria. He finds that Berkshire Hathaway ticks all the boxes: it is a high quality business selling at an attractive price with excellent management and a low risk of permanent capital loss. Each of Berkshire Hathaway’s underlying businesses contributes to the investment case and our strong conviction in the superior return this investment will likely generate for our clients.

Berkshire Hathaway has consistently outperformed the S&P 500 Index since the late 1980s

Berkshire Hathaway has grown its net asset value (NAV) by 19.0% per annum (p.a.) since 1965, matched by share price appreciation of 20.8% p.a. This is a significant outperformance of the S&P 500 Index, which delivered 10% p.a. over this period, as shown in Chart 1.

Berkshire Hathaway is a quality business and meets all of our investment criteria

Cadiz Asset Management (CAM) defines a good investment as a business that delivers a superior real return at a very low risk of loss. Ideally, we prefer a low probability worst-case scenario where the investment suffers no or low capital loss. To achieve this, we predominantly invest in high quality businesses with good management that are selling at an attractive price with low financial and operational risk.

Berkshire Hathaway’s underlying businesses consist of insurance operations, energy operations, railroads, and a whole host of manufacturing, retail and service businesses as well as financial services businesses (secured lending and fleet leasing). The company also has a large investment portfolio of high quality businesses. We’ve included a brief discussion of the key businesses:

The insurance business provides insurance only when it is profitable

The nature of the insurance industry is that these businesses receive money today with a promise to pay in the future when the risk event occurs. The official term for this is ‘float’. Insurance businesses can invest this float and keep the return on investment, which causes the industry as a whole to write business at a loss. Berkshire Hathaway’s insurance business is cautious about writing profitable policies and has earned an average underwriting profit of $1 434 per share over the last 10 years, with no underwriting losses. In addition, the fact that two of the best capital allocators – Buffett and Munger are in charge of the float has resulted in a very good investment return.

The energy business benefits from Berkshire Hathaway’s credit rating and economies of scale

Berkshire Hathaway’s excellent credit rating enables the highly regulated energy business to have a low cost of capital. The business has also shown the ability to operate efficiently and lower the cost of energy for consumers, which regulators appreciate and encourage. In addition, the large fixed cost of power plants limits competitors, allowing the business to benefit from economies of scale. These factors all contribute to a fairly stable operating environment with consistent returns.

The railroad business benefits from a lack of competition

Berkshire Hathaway’s railroad business also benefits from economies of scale since there are usually only two rail operators in any region in North America. In addition, rail is the low-cost option for transporting goods, and cannot be replicated by other forms of transport. The only exception is transport by barge, but this is only viable where the transport route follows a major waterway.

The manufacturing, retail and service businesses generate high return on tangible capital

These businesses either operate in niche markets or have brand and other intangible assets. They use their brand power to charge a higher price for better quality products or operate a very low-cost business model to generate superior profitability. Together these businesses have sufficient barriers to entry with diverse operations that are considered sustainable.

The financial service businesses operate in niche markets and have very good reputations

In addition, they have the back-up of Berkshire Hathaway’s balance sheet. These businesses therefore use a low-cost model to maintain and improve their market share at similar or better profitability than their competitors. Berkshire Hathaway also instils a culture of only making loans to clients who will be able to pay back the loan in full, which limits bad debt write-offs.

Berkshire Hathaway is not exposed to any single risk

The diverse, well-managed underlying businesses reduce the potential of permanent capital loss significantly. In fact, there is no single risk that could significantly impair the underlying businesses’ profitability in the near future. According to Buffett, only a major global catastrophe or horrific terror attack could cause a material loss. This risk, however, applies to the global economy and is not specific to the company or its underlying businesses.

Management has a 50-year track record of superior capital allocation

Buffett and Munger have an excellent track record of over 50 years of superior capital allocation and are thought leaders on investing and business management. Berkshire Hathaway does not have a share option scheme and Buffett earns only $100 000 a year. Management has almost all of their wealth invested in Berkshire Hathaway shares, and their interests are aligned with minority shareholders. They run the business in a frugal manner, with only 25 people employed at the head office. In addition, Buffett doesn’t interfere with the CEOs and management of the underlying businesses. In fact, he rarely speaks to them unless they call him with a question.

Due to the age of the management team (Buffett is 85 years old and Munger is 92), succession planning has long been cited as a key risk. However, Buffett has implemented a well-defined succession plan with two co-investment managers who have excellent track records. Two of Berkshire Hathaway’s current subsidiary CEOs have been identified as potential candidates to take over as CEO, and Buffett’s son will take over the role of chairman.

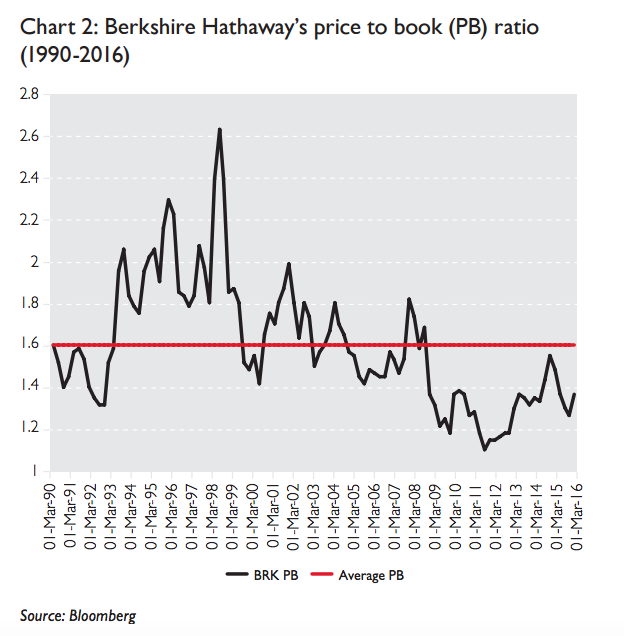

The attractive price offers a large margin of safety

The last piece of the puzzle is the price, and Berkshire Hathaway is currently very attractively priced at a price to book ratio (PB) ratio of 1.3X, as shown in Chart 2. There is also the backstop of the company’s ability to buy back shares at or below a PB ratio of 1.2X, which is too cheap according to Buffett.

We are confident that our significant holding in Berkshire Hathaway will benefit our clients

Berkshire Hathaway is a good quality business with high sustainable return on tangible capital, an excellent track record and fantastic management. It is very attractively priced, with low risk of permanent capital loss. Berkshire Hathaway is therefore an ideal candidate for a large investment position, and we are optimistic that, as our single largest offshore investment, it will benefit our clients.

- Razeen Dinath is a qualified chartered accountant and graduated from UCT. He completed his articles in the financial services division of PWC. He then joined Allan Gray where he gained experience in investment analysis and risk management. He further developed his investment analysis skill at RECM. Prior to joining Cadiz Asset Management as a senior Equity Analyst he was part of the unconstrained investment team at Momentum asset management. Razeen has 10 years post article experience in asset management.