The newly listed Twitter has had an exciting first day out on the market. The Twitter IPO was priced at $26 a share, but opened at over $45 on the New York Stock Exchange on Thursday. After a volatile day of trading, the share closed at $44.90 – an impressive performance overall. But what is Twitter really worth? After all, so far the company has failed to turn a profit, failed to generate stable growth, and failed to offer a plan for achieving profitability. Given all that, it’s hard to see why the market thinks the company is worth $32bn. In this fascinating piece from the Wharton business school at the University of Pennsylvania, top business professors give their view on the proper way to value Twitter, and on what the company is really worth. – FD

Every day, Twitter’s more than 230 million active users send out about 500 million 140-character word dispatches about everything from daily specials at local restaurants to minute-by-minute accounts of political and social strife happening around the world. But questions about the true financial worth of all this information, and whether Twitter can turn it into a robust, sustainable source of revenue, has dogged the company since its inception in 2006.

The company faces a judgment day of sorts on Thursday, when Twitter makes its debut as a public company. Twitter’s IPO comes after heavily hyped, but ultimately problematic, initial stock market showings from fellow social networking firms Facebook, Groupon and Zynga. Yet even if Twitter makes a big splash, is it a good buy for the long term? Wharton experts are mixed in their views, noting that while tech firms have huge advantages — robust user bases among them — they also come with some potentially serious deficits.

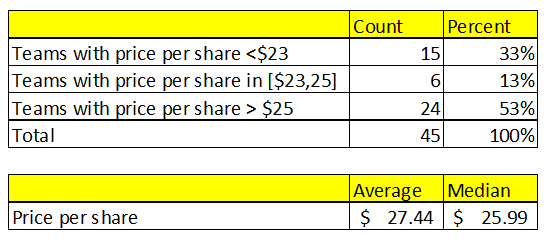

In the weeks leading up to Twitter’s IPO, Wharton finance professor Luke Taylor asked students in one of his classes to do their own research and come up with what they felt was a fair valuation for the company. Two-thirds believe that the company’s expected initial public offering price range of $23 to $25 per share was fairly valued. [Editor’s Note: According to news reports late today, Twitter has set the price at $26 a share.]

Taylor notes that out of his 161 students, 13% believe Twitter’s price should be between $23 and $25 while 53% said the stock would be fairly priced even above $25. When taking all of the student analyses into consideration, the average fair price per share was $27.44 while the median came to $25.99. The estimates of both MBA and undergraduate students were close, at $25.99 and $25.60 respectively.

“Twitter at $25 per share is a good investment,” says Taylor, who demonstrated his confidence in the students by placing an order through his brokerage to buy 400 shares of Twitter stock at $23 to $25 per share for an estimated total cost of $10,000.

The last big social network to go public, Twitter will debut on the New York Stock Exchange with the ticker symbol “TWTR.” The company initially set a price range of $17 to $20 per share, but due to high demand, raised it to $23 to $25 this week. However, it ultimately decided against expanding its offering size of 70 million shares with another 10.5 million in overallotments. Twitter closed its order books a day early as well. It is expected to establish the IPO price late Wednesday.

Wharton management professor Raphael (Raffi) Amit says Twitter is going public when investor enthusiasm is high for such debuts. “It’s a hot market for IPOs,” he states, noting that the third quarter of this year had 25 initial public offerings, more than double the figure for the same quarter in 2012. Driving demand are low interest rates, investors seeking higher returns and a greater confidence in the economy and its prospects, Amit adds.

He suggests that the market is not in a tech bubble like it was at the peak of the dot-com boom. The pace of today’s IPOs still falls behind that of 1999 and 2000, when there were 280 and 238 venture-backed IPOs respectively, according to the National Venture Capital Association. Also, the median valuations of pre-IPO companies backed by venture capitalists are not “substantially higher” today than historical norms, Amit points out. In the first half of 2013, he says, the median was $300 million. That compares to $362 million last year, and from 2008 to 2011, the valuations ranged from $238 million to $383 million.

Art over Science

Valuations of Twitter by Taylor’s students ranged from $500 million to $33.7 billion, showing how difficult it is to gauge a company that has no history of earnings reports and a business model that remains largely unproven. “This is an art, not a science,” Taylor notes. “Even forecasting revenue out for five years is incredibly difficult.”

Taylor gave his students the assignment weeks ago and could not have reverse-engineered their reports because Twitter just raised its IPO price range this week. They were told to forecast Twitter’s five-year revenues, profit margins and cash flows, and find comparable companies on which to base their valuations. The students were divided into more than 40 teams.

Abhijeeth Ramesh, a 21-year-old senior, projected that Twitter has an enterprise value of $14.9 billion or $27.35 per share. He and his teammate Aditi Abrol looked at Facebook, LinkedIn, Google and Yahoo as the closest peers to Twitter and based their assumptions on the companies’ performance and financial metrics. Specifically, they considered the early post-IPO performance of Facebook and LinkedIn as indicators of how Twitter might do in the early days as a public company. Ramesh and Abrol also turned to Google and Yahoo because they are mature companies that are heavily reliant on advertising. The students thought the margins of the two more established firms would be helpful in modeling what Twitter’s results would look like years down the road once it has stabilized.

Ramesh and Abrol expect Twitter’s year-over-year revenue growth to steadily drift down, from 88% in 2013 to 17% in 2018. They see operating profit turning positive in 2015 and free cash flow to be in the black in another three years. “Our fundamental approach was to stay a little conservative,” Ramesh says. It seemed the most prudent approach, he notes, since Twitter did not disclose advertiser metrics such as how many users are on the platform and their churn rate. Advertising is the core driver of revenue, so these disclosures are critical for modeling projections. “It was the most crucial piece of information, and [Twitter] didn’t provide it,” Ramesh points out.

A look at how Wharton students in Luke Taylor’s class valued Twitter.

The two students have a “buy” rating on Twitter because the IPO price range is below their fair value of $27.35. But Ramesh says he is not going to be buying the stock out of the gate. “I would be cautious until they reveal more of their revenue model,” he notes, adding that he predicts Twitter shares will go up on the first day of trading but then eventually float down over the next few months.

An Uncertain Path

Wharton marketing professor Pinar Yildirim says an uncertain path to profitability is a problem for many technology companies. “Many tech firms gain instant popularity and a large user base with very few opportunities for monetization,” she notes. “They often just have popularity, not necessarily profitability.” The challenge with social media companies in particular is that the more they try to make money from their large user bases, the greater the consumer backlash, as users bristle at seeing their feeds clogged with an increasing number of ads or their dispatches used for promotions, Yildirim points out. Moreover, many of these firms rely on advertising but advertisers may see them all as the same when it comes to reaching their target customers.

For Alec McCullie, a Wharton MBA exchange student, the toughest challenge in valuing Twitter was finding stable, comparable companies. There are only a handful of social networks, and each one has different characteristics with multiples that can vary widely. He and his team valued Twitter between $14 billion and $21.2 billion. Shares trading between the mid- to high-20s are “probably reasonable,” says McCullie, who is bullish about Twitter and the emerging social media sector. “It could be the next Google in terms of how people get their information.”

Tingyan Jia, a Wharton undergraduate, says the toughest part for his team was coming up with a market size. “Market sizing is of vital importance for any valuation and is especially hard for fast-growing high-tech companies like Twitter,” he notes. Like McCullie, Jia says it was difficult to find companies that are comparable to Twitter. The social network had economies of scale because of its wide reach, which rules out younger peers, but it also has a modest market cap that is far smaller than those of Facebook and Google. In the end, his team decided to use Facebook, LinkedIn, Google and Yahoo as the closest peers to Twitter — something other teams did as well. Jia’s team values Twitter at $13.5 billion, or $24.75 per share.

Valuing social media companies like Twitter can be difficult because it depends heavily on the underlying assumptions, which can vary greatly, students note. For Twitter investors, another worry is whether the IPO can avoid a fiasco like Facebook’s. “Investors might be a little more careful about what to expect,” Yildirim says. “But Twitter is certainly looking promising because they have not yet tapped into their potential.”

Published: November 6, 2013 in Knowledge@Wharton

Republished with permission from Knowledge@Wharton (http://knowledge.wharton.upenn.edu), the online research and business analysis journal of the Wharton School of the University of Pennsylvania.