EDINBURGH — Peregrine has declared its first interim dividend and holds the promise of more for shareholders. That’s the assessment by a team of analysts who work under the pseudonym of John Maynard. In this analysis, Peregrine is put under the microscope, with the conclusion that Peregrine is one of the most under-rated mid cap stocks. Although revenues and profits are lower than in the previous reporting period, there are signs that the investment specialist is set to improve its performance. It is focusing on growth in recurring fees rather than performance fees and its offshore focus is expected to overshadow its activity in the South African market. Crucially, Peregrine also targets the very wealthiest individuals, who are less vulnerable to economic challenges than the market that competitor Coronation focuses on. – Jackie Cameron

By John Maynard*

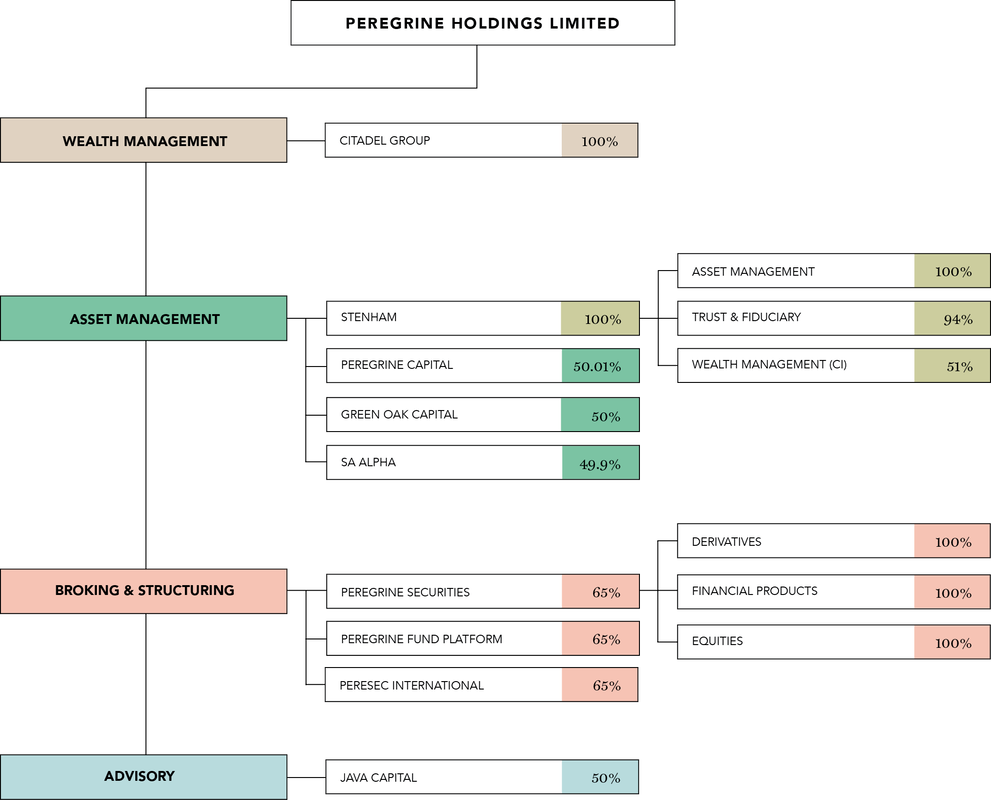

About Peregrine Holdings

Peregrine Group, one of South Africa’s premier wealth & alternative investments specialists. Peregrine is a leading financial services group that caters to the financial needs of both individuals and institutions, and offers best-of-breed investment management solutions and advice. Founded in 1996, the Peregrine Group comprises a number of diversified, industry leading, financial services businesses, including Citadel Holdings, Peregrine Capital, Peregrine Securities, Stenham, Green Oak Capital and SA Alpha. Peregrine also owns 50% of Java Capital, which is widely regarded as the premier independent corporate advisory house in South Africa.

Over the past two decades, Peregrine has earned a reputation for delivering consistently high levels of risk-adjusted returns over both the medium and long-term, even in difficult market conditions, a snapshot of which is evidenced in the Five Year Review. This is primarily driven by Peregrine’s resources and personnel, which the Group regards as being of unrivalled calibre. Wealth created by Peregrine Group amounted to R1,76 billion for the year to 31 March 2018 (2017: R1,74 billion). Distributions to stakeholders are set out in the Value Added Statement. Driven by an owner-managed and entrepreneurial culture, Peregrine invests on behalf of its clients, facilitates investments and provides comprehensive advice across four business segments:

- Wealth Management;

- Asset Management;

- Broking and Structuring; and

- Advisory.

Through its various subsidiaries, Peregrine can draw on an enviable field of expertise in private client wealth management, global funds-of-funds, single manager hedge funds, broking and structuring, trusts services, corporate finance and advisory services, as well as foreign exchange and treasury management. In addition to this, the Group is committed to good governance and transparency, which has generated a business model that is well-respected by partners, peers and clients, and is recognised for its quality by the financial services industry at large. Peregrine listed on the JSE, under the Financial Services sector, in June 1998, and, as at 31 March 2018, had a market capitalisation of R4.7 billion. The Group is responsible for some R103 billion in total gross assets under management and or administration/advice. The Group focuses predominantly on operating financial services businesses in South Africa, the United Kingdom and the Channel Islands, and employs more than 750 individuals across its operations. The South Africa business maintains an appropriate and sustainable B-BBEE shareholding via Peregrine SA Holdings.

The image below shows Peregrine’s Group structure

Financial results

So lets take a look at some of the key numbers in Peregrine’s financial results:

- First ever Interim Dividend : 85c a share (which places them on forward dividend yield of 8.3%)

- Headline earnings per share R1.28 (up 5% from R1.22 in prior year), which places the group on a forward PE of 7.99

- Operating revenue: R788.9 million down 5% from R828.6 million in prior year

- Profit for the period: R341 million, down 6% from R363.7 million in prior year

- Net asset value per share: R10.98 (so trading around double its NAV), which is to be expected from a operating entity

- Cash generated from operations per share: R0.91 a share

- Cash and equivalents: R2.005 billion (or R8.88 per share).

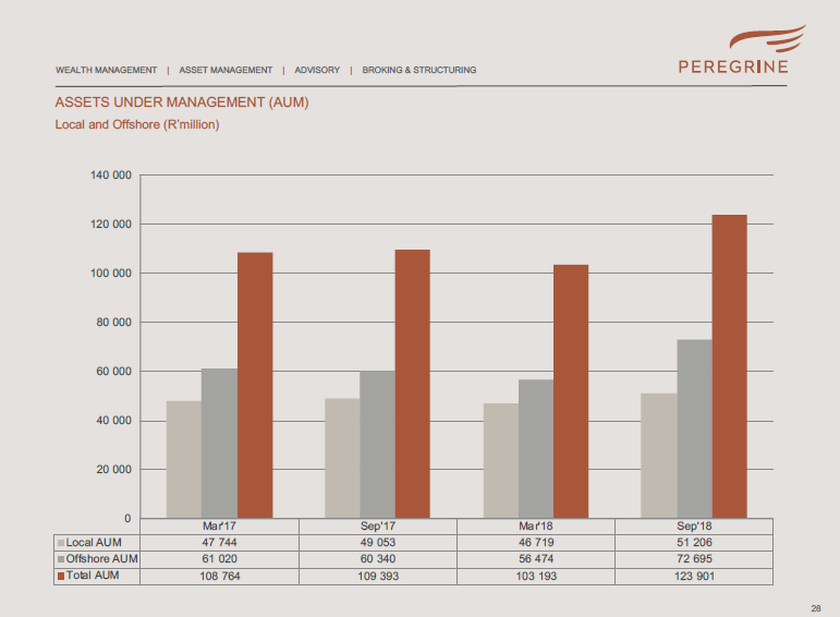

So we saw yesterday that one of the biggest local asset managers, Coronation Fund Managers currently has around R587 billion in assets under its management. So how much money does Peregrine manage? The image below shows a breakdown of Peregrine’s assets under management of both their local and offshore operations.

So locally, Peregrine has R51,2 billion in assets under management (AUM) as at end of September 2018. Thats a bout 8.7% of the assets that Coronation has under its management. So they are a lot smaller than Coronation for example. But Peregrine caters for a smaller niche market (the very wealthy) whereas Coronation targets the every day retail investors. Including Peregrine’s off shore assets under management the group manages R123.9 billion in assets. Their total assets under management is about a fifth of that of Coronation.

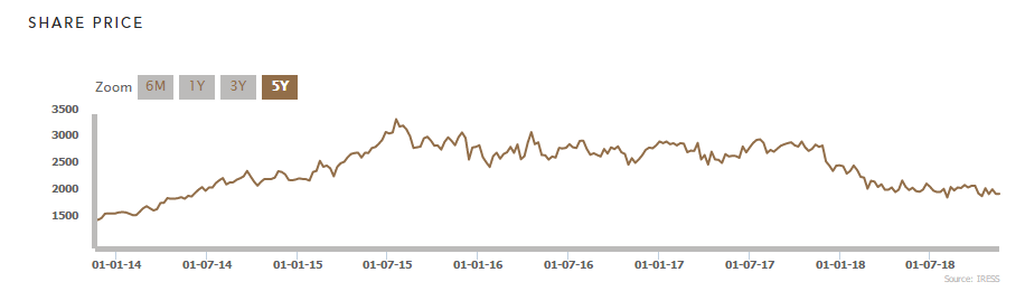

Peregrine (PGR) share price performance over last 5 years

Peregrine (PGR) share price for the last 5 years

The image above shows the share price performance of Peregrine Holdings (PGR) over the last 5 years. And while the share price climbed substantially from the 2014 levels of around R15 a share to close to R35 in 2015, it has been in a slow steady decline since then and is currently trading at just above R20. As we showed yesterday with Coronation Fund managers, the share price performance of asset managers has been under significant pressure due to less performance fees being earned due to weak market conditions. But PGR has over the years focused on increasing recurring earnings instead of depending on massive performance fees. In this set of results recurring earnings made up 91% of their earnings.

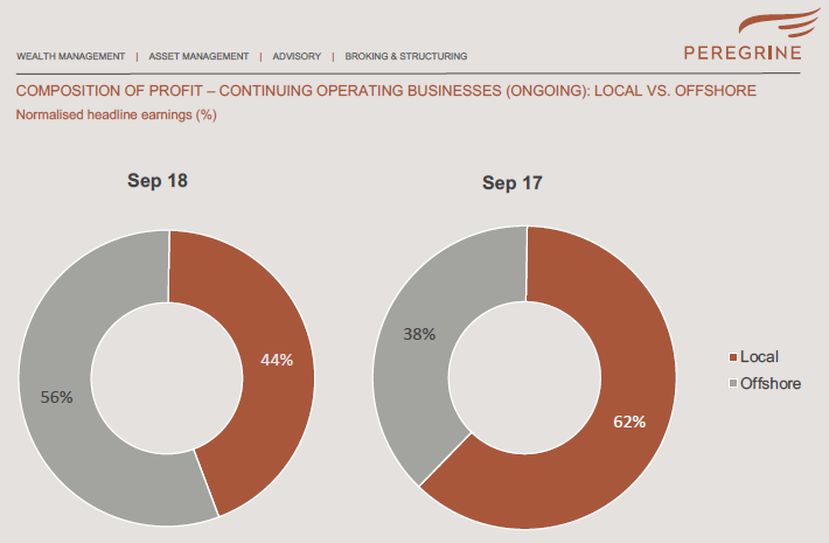

We like the fact that a large chunk of PGR’s earnings is earned outside of South Africa, which provides some Rand hedge benefits for the group and investors in the company. The image below shows the composition of PGR’s earnings between South African operations (local) and their offshore operations.

For the 6 months ended September 2018, 56% of PGR’s earnings came from their off shore operations, while this was only 38% in the prior year. Either their offshore operations are pumping or their local operations are really struggling. Lets take a look at managements commentary to see if they mention whether its SA operations struggling or their offshore operations that are booming.

Management commentary on the financial results

The six months ended 30 September 2018 could best be summarised as an emerging market risk-off sell-off with safe haven assets and geographies having outperformed riskier assets with growth potential. On the international front, there was accelerated growth in the US on the back of fiscal stimulus as well as reduced commodity demand from China, which resulted in currency depreciation against the US Dollar in many emerging markets and developing economies with Argentina, Turkey, Brazil and South Africa being amongst the worst affected. Likewise, the US Dollar was stronger against the Euro, Sterling and Yen.

Locally, the South African economy slipped into a technical recession during the second quarter of 2018. The possibility of credit-rating downgrades will continue to hang over the economy well into next year with fiscal slippage and a slow-moving reform agenda likely to constrain growth over the medium-term. The recent appointment of Tito Mboweni as the new Minister of Finance represents a step forward in President Ramaphosa’s administration’s fight against corruption. Notwithstanding the difficult trading environment, the operating businesses in the Group increased Segmental earnings to R283 million with the continuing operations (those businesses excluding the Broking & Structuring business, which is in the process of being sold), delivering growth of 31% to R206 million.

Across the continuing operations, on a Segmental basis, annuity earnings grew by 15% and accounted for 91% (2017: 75%) of the aggregate earnings. Variable and performance fee earnings decreased by 67% to R13 million mainly due to lower performance fees earned by Peregrine Capital. The contribution from offshore operations continues to play a meaningful role in diversifying Group income with 56% (2017: 38%) of the aggregate earnings from continuing operations being generated from outside of South Africa. The above mentioned annuity earnings and contribution from offshore operations relate to Segmental earnings and excludes a one-time performance fee on exit amounting to GBP3 million (R58 million) received by Stenham during the period arising out of the disposal of a property which formed part of the property portfolio sold to Stenprop in 2014 (“the ad hoc performance fee”).

While the South African economy remains beset with difficulties, we are encouraged by the actions taken by the current leadership. We believe they will translate into higher levels of confidence initially, and potentially higher levels of investment into the economy which will promote growth over the medium to long term. We are also more optimistic about the outlook for the major South African asset classes which, following a period of very disappointing returns, are presenting above-average opportunities to long-term, valuation-driven investors such as ourselves. The outlook for global asset classes is more mixed, which too has enabled us to construct differentiated portfolios.

We remain optimistic that the current positioning of our strategies will generate higher future returns for our clients. Together with our increased investment in our infrastructure, technology and people over the past year to support the provision of world-class service to our clients, we believe this will ensure the delivery of sustainable long-term value for all stakeholders.

Peregrine (PGR) share valuation

Sure the markets performance over the last few years have not been great, and by virtue of that PGR has been earning less in performance fees. But on the positive side it is good to see their focus on improving recurring earnings to ensure their earnings are less volatile over time. This not only helps them in planning and predicting future earnings and profits, and can plan ahead for the company from a more solid and stable earnings base, but it also assists the market in valuing the business and estimating or predicting its earnings.

We have always loved Peregrine (PGR) and we believe it is one of the most under rated mid cap shares around. We like the fact that they have introduced their first ever interim dividend. They earn a large chunk of their earnings outside of South Africa. They have a very strong balance sheet, with around 40% of the share price being made up by cash. We like their cash generation capacity, greater percentage of earnings earned from recurring earnings and not performance fees. A greater business focus on what they are good at, which is asset management and wealth management (basically we happy they got rid of their property portfolio).

Based on their current financial results, their PE ratio and dividend yield, we value the group at R24.69, which will place the group on a PE ratio of 9.6 (which is not demanding at all, even with the poor performing market) and a dividend yield of 6.9%.

- John Maynard is the nom de plume of an independent economist who is obsessed with official statistics – and uses these facts to blast through misleading narrative and propaganda. For more of his unique insights click here.