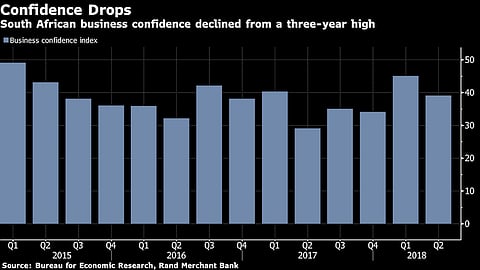

The RMB/BER business confidence index fell to 39 from 45 in the prior period, FirstRand Ltd.'s Rand Merchant Bank unit and the Stellenbosch, South Africa-based Bureau for Economic Research said in an emailed statement Wednesday. This means three fifths of the 1,700 respondents now regard prevailing business conditions as unsatisfactory.

Briefs

Business confidence deteriorates in Q2 as economic realities stifle Ramaphoria

After surging from 34 to 45 in the first quarter, the RMB/BER Business Confidence Index deteriorated to 39 in the second quarter of 2018.

RMB media statement:

After surging from 34 to 45 in the first quarter, the RMB/BER Business Confidence Index (BCI) deteriorated to 39 in the second quarter of 2018. This means that close to three fifths of respondents now regard prevailing business conditions as unsatisfactory – a disappointing outcome, yet probably an accurate reflection of reality.

The second-quarter survey was conducted between 7 May and 5 June, and included 1,700 business people in the building, manufacturing, retail, wholesale and new vehicle trade sectors.

Figure 1: RMB/BER Business Confidence

Source: BER, SARB (Shaded areas represent economic downswings)

Details

The first quarter's 11-point jump in the BCI was owing mainly to the euphoria surrounding the change in the country's political leadership in February. Yet, as we noted at the time, it would be unusual for confidence to be sustained after such a significant jump. Moreover, we felt that as the excitement was likely to wear off, and the reality of still subdued economic activity kicked in, confidence would soften in the second quarter.

Our intuition has proved to be correct. Not only did business activity remain disappointingly weak – worsening even, in some sectors – but "Ramaphoria" also faded in the wake of the ever-rising petrol price, the political debate around "expropriation of land without compensation" intensifying, and growing signs that the strong synchronised global economic upswing has started to fizzle out. Consequently, despite still low inflation and, related to that, low interest rates, business sentiment deteriorated in four of the five sectors making up the RMB/BER BCI.

Ramapanther. More cartoon magic available at www.zapiro.com.

After jumping from 34 to 41 in the first quarter, building contractor confidence retracted to 37 in the second quarter. This happened notwithstanding continued and improved activity in the non-residential sector – albeit from heavily depressed levels. Building activity in the residential property market changed very little in the second quarter.

Following a large 13-point rise to 42 in the first quarter, retail confidence retreated to 33. Clothing retailers experienced seemingly better trading conditions during the second quarter, with food retailers continuing to see a recovery in sales relative to last year's dismal performance. By contrast, recent noticeable growth in the sales volumes of furniture, appliances, building materials and other durable goods just about came to a halt in the second quarter.

New vehicle dealers also witnessed a noticeable worsening in sales, possibly because consumers had brought their purchases forward to the first quarter to pre-empt paying even more, given the 1% hike in the VAT rate on 1 April – a dynamic that is likely to also have affected retailers selling other expensive consumer goods. Dealer confidence dropped from 52 index points to 35 in the second quarter.

A striking deterioration in demand knocked manufacturing confidence from 37 to 27 in the second quarter – a drop that almost wiped out all of the first-quarter improvement in sentiment. Disconcerting is the fact that domestic as well as export sales volumes slackened. And production volumes did not fare much better.

The exception in the second quarter were wholesalers. Their confidence jumped from 53 to 62 in the second quarter. We find this upturn difficult to explain, which makes us doubt its staying power.

Bottom line

Despite the second-quarter decline in the RMB/BER BCI, the trend in business confidence remains upwards, even if only tentatively so. To help preserve and make this increase more of a lasting one, it is important that the political and policy factors currently weighing down on confidence are resolved. In this regard, it certainly would help if the (unnecessary) uncertainty that surrounds both the Mining Charter and the government's land reform plans is settled. Delivering on the government's stated priorities of, for example, removing the remaining bottlenecks in the telecommunication and tourism sectors would be a significant step to further boosting confidence and helping lift GDP growth onto a higher trajectory.

"Acting on these initiatives cannot happen soon enough. This is especially so considering that global headwinds are mounting and domestically, the inflation as well as interest-rate cycles have, in all likelihood, bottomed out" said Ettienne Le Roux, chief economist at RMB.

South African Business Confidence Falls as Ramaphoria Wanes

So-called Ramaphoria has faded in the wake of record-high gasoline prices, the intensifying political debate around expropriation of land without compensation, and growing signs that the strong synchronized global economic upswing has started to fizzle out, they said.

Ramaphosa's rise to power since December initially boosted sentiment and the rand following Jacob Zuma's scandal-ridden tenure of almost nine years. The currency is now at the levels last seen before Ramaphosa replaced Zuma as leader of the ruling party and the statistics office said last week the economy contracted the most in nine years in the first quarter.

The trend in business confidence remains upward, RMB and the BER said. To sustain this, political and policy factors that weigh down confidence, such as the Mining Charter and the government's land-reform plans, must be resolved, they said.

"Acting on these initiatives cannot happen soon enough," said Ettienne Le Roux, chief economist at RMB. "Global headwinds are mounting and domestically, the inflation as well as interest-rate cycles have, in all likelihood, bottomed out."