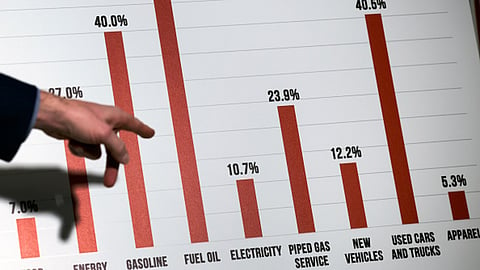

In a whirlwind of economic data and monetary policy shifts, this week's focus rests squarely on US inflation, a metric with profound implications for markets and consumers alike. As central banks contemplate rate cuts amidst mixed economic signals, the legacy of investing luminary Jim Simons leaves an indelible mark, his groundbreaking strategies defying conventional wisdom. As we navigate this landscape of uncertainty, understanding the past may illuminate the path forward..Sign up for your early morning brew of the BizNews Insider to keep you up to speed with the content that matters. The newsletter will land in your inbox at 5:30am weekdays. Register here..By John Authers.Today's Points:.Yes, this week's US inflation numbers matter — a lot.Politics do affect consumer confidence, but the message from Michigan is valid.Central banks are in a mood to cut rates — and Sweden's Riksbank did.AND Rest in Peace, Renaissance Man Jim Simons. .___STEADY_PAYWALL___.Inflation Elation.Here we go again. Brace for the latest dose of critical data on US inflation over the next three days, as the New York Federal Reserve publishes its monthly survey of consumers' inflation expectations Monday, followed by the Labor Department's report on producer prices Tuesday and consumer prices Wednesday. These reports will matter a lot..Of late, the mood has switched toward optimism that inflation is being tamed, while central banks that met last week either reduced benchmark interest rates, or suggested cutes were imminent. The latest data also show a US economy slowing in just the way the Federal Reserve wants to see. The jobs market has stayed obdurately strong throughout the post-pandemic fight against inflation. That makes it far harder for a central bank to be lenient. But last week, initial US claims for jobless insurance spiked to their highest level since August:.This is a noisy series, and last week's result followed several low numbers, so the four-week moving average of claims remains in its recent healthy range. But a rise in claims like this is exactly what we would expect to see if higher rates were indeed beginning to slow the economy; if they continue to run at this level for another month, it would be far easier for the Fed to justify cuts..Read more: Frozen US housing markets and inflation – are high interest rates keeping inflation elevated? .Meanwhile, the latest edition of the University of Michigan's long-running survey of consumer sentiment showed a startling drop in both expectations and assessments of current conditions. Such negativity — when many in the market were braced for a strong "no landing" economy — came as a shock. It's statistically significant. Again, numbers like this make rate cuts much easier to justify: .The problem, as with so much else in 2024, lies with politics. Polarization has led to a wide divergence in economic perceptions. Republicans think things are terrible; Democrats think they're great. This is how consumer confidence has moved over the last two presidential terms, broken down into the opinions of Republicans, Independents and Democrats:.The divergence after the 2020 election is extraordinary, showing a deep lack of confidence in both major parties. But it's not clear that partisanship is distorting the overall numbers. Republicans, Independents and Democrats are all in agreement that things are roughly as good now as they were in November 2016, before the Trump era began. Independents, whose views are presumably least swayed by politics, are not back to their pre-pandemic levels of confidence. Overall, even once political leanings are taken into account, these numbers suggest that consumers perceive a weaker economy than the official numbers..Read more: Investors adapt to lingering inflation: Wealth managers see opportunities amid uncertainty.Why is this? Points of Return has shown in recent weeks that "anti-core" inflation, of just energy and food, went through a big change in 2022 that will have a lasting effect on consumer budgets, particularly for lower income households. There's a fair case that neither presidents nor central banks can do much about food prices, but it's still a problem and it still influences perceptions. .Then we come to the biggest fly in the ointment. The Michigan survey on expected inflation was higher than forecast and sparked a rise in short-term bond yields. This is the level of inflation consumers have expected for the following 12 months, divided by political identity:.Again, the effect of partisanship is clear, but it's not obvious that it matters much. They all move in the same direction, with expected inflation peaking (at very different levels) in the summer of 2022. People of all political persuasions now expect much the same rise in prices as they did at the time of the last presidential election. Independents' expectations are close to 3%, the lowest in more than three years..Then there are the extraordinary results when Michigan asked for forecasts of average inflation over the next five to 10 years. The university publishes both a mean and a median number, and the latter is more widely followed. Given that very few people ever expect prices to go down, outlying high inflation expectations will inevitably skew the mean upward. It's also true that consumers have long been too negative, and the median has never dropped to the 2% target in the last three years..All that said, it's quite something that mean longer-term inflation expectations are now above 5% for the first time in three decades. .There's a significant mass of people who are convinced that inflation rates are going to rise a lot from here. They probably think so in large part because of their ideological framing, but that doesn't make their expectations any less real. Long-run expectations have been well anchored for a long time, and it's strange to see them loosen now, rather than when inflation peaked two years ago. This number is probably a fluke, but until we can say that for sure it does make it harder for the Fed to ease monetary policy..Read more: 🔒 Central banks to pursue cautious rate cuts as inflation concerns linger.All of this leaves the situation in fine balance as we await Wednesday's Consumer Price Index. After three successive negative surprises, economists polled by Bloomberg News are confident that core inflation will be down. Even the highest estimate reported to Bloomberg was lower than the March figure. That's encouraging, although the corollary is that an upside surprise would really hurt:.As for the core US markets, both bonds and stocks had an unusually quiet week heading into this data. The S&P 500 Index is just below its peak in March, with traders reluctant to take too strong a position ahead of the April inflation data. If the numbers are in line with or below estimates, the stock market will probably rally to new highs. If not, well, not. .Rates Descent.And then there were two. The Riksbank, Sweden's central bank, last week became only the second developed market central bank – after the Swiss National Bank — to cut its policy rate. It did so in response to persistent economic weakness. After four consecutive quarters of contraction, Riksbank Governor Erik Thedeen was moved to act, while confident that inflation, which peaked at 10% in 2022, was on its way to the 2% target. The 25-basis-point cut in the benchmark rate, the first in eight years, follows an aggressive post-pandemic hiking cycle which pushed the rate to 3.75%..Will other central bankers, especially in countries with distressed economies, take a similar path, and jump ahead of the Fed to loosen monetary policy? As Points of Return has said, here and here, central bankers face grave dangers in lowering rates..How far the Riksbank goes will depend on the Swedish krona. This year, it's down by about 4.5% against the euro – and 15% since late 2021. It's now approaching its all-time low against the common currency set last year. Gavekal Research's Cedric Gemehl argues that the Riksbank might be circumspect about further rate cuts, lest they lead to more krona depreciation and stoke inflation via the higher cost of imports..Read more: 🔒 Argentina's president Javier Milei faces economic turbulence as inflation soars .That said, the krona took last week's rate cut relatively in stride. That will be encouraging for Thedeen, but analysts at Bank of America agree that the Riksbank will take a cautious approach toward further cuts:.The Riksbank showed some independence from the large central banks, but we still doubt that a clear/persistent divergence is a realistic possibility. We expect the data flow to continuously test the (limited) credibility of the "three cuts" guidance – incoming data, especially on the inflation side, is likely to remain dovish in the next few months. With FX concerns now taking a back seat, we see significant risk of an acceleration in the cutting cycle. .If all goes to plan, the policy easing should lift the services sector of the Swedish economy, which, unlike manufacturing, remains in contraction. This Gavekal chart offers a glimpse of the challenge the rate cuts are meant to address:.After Sweden, the Bank of England may be up next. Governor Andrew Bailey last week expressed more confidence inflation was coming under control, meaning a rate cut is only a matter of when. June is the next opportunity. Bloomberg Intelligence's Dan Hanson and Ana Andrade argue that by then, all the evidence required for the BOE to commence rate cuts should be in place, through two CPI prints. If overnight index swaps are to believed, as measured by the Bloomberg World Interest Rate Probabilities function, then there's a 50/50 chance of a cut then, and it's a virtual certainty that the BOE will have cut by its August meeting. Bank of America's analysts, however, maintain a base case for a fall cut. Stickier wages, they argue, will delay a cut until then and subsequently limit them to one per quarter throughout 2025:.Read more: SARB Governor is working on lowering the country's 3-6% inflation target range.The latest UK earnings data, due this week, could be crucial, and might yet stay the BOE's hand. Analysts at Bank of America worry that the BOE may be tempted to go faster and earlier with rate cuts while inflation expectations are still "not-perfectly anchored." "That would risk bringing back some of those unwelcome developments and stop the central bank well above where we have them going today in terms of rates," the firm's strategists wrote in a research note. .Countries where high rates have wreaked economic pain have a sense of urgency about easing monetary policy. But there's an even more pressing need to ensure that gains made in bringing inflation rates from their peaks are not lost immediately. It's a difficult balancing act. And, as we await another series of US inflation data, nothing is guaranteed. .Richard Abbey.The Renaisssance Man.Farewell to the investment world's Renaissance Man. Jim Simons, the founder of Renaissance Technologies whose Medallion fund was quite possibly the most successful investment vehicle of all time, passed away on Friday at 86. One of the giants of finance, his record was a retort to efficient market theorists who held that it was impossible to beat the market consistently without luck. After averaging a return of 66% per annum for some decades, Simons made such arguments look silly. But nobody could copy him..Unlike the other pivotal figures in investment, such as Warren Buffett and Charlie Munger, George Soros, Peter Lynch, Jack Bogle or Ray Dalio, Simons avoided publicity. Interviews with him were rare, and he never presented his investment ideas in a book. And as his fund was exactly what people have in mind when they talk of a "black box," it's not possible even to assess the trades he made; nobody outside his firm knows exactly what they were. .We know what he did in general terms. Renaissance gathered a staggering amount of data, used exceptionally difficult mathematics to find trends and anomalies, and then traded them rigorously and quantitatively. This was unique when Simons started out, but is widely adopted practice now. Nobody has managed to replicate what Simons accomplished with equal success, although many have used quant investing to become very rich. .Read more: 🔒 Boardroom Talk – Bulls are back on Wall Street after inflation falls more than expected.Why is that? Scale might have something to do it. While Medallion, which isn't widely offered, is spectacularly successful, returns generated by other Renaissance funds offered more widely were much more similar to other big quant funds. The bigger you are in investing, the easier it is for others to see what you are doing and take evasive action and, in general, the more risks you have to take to move the returns needle. .There may also have been a first-mover advantage. Once someone spots a market inefficiency and moves to exploit it, the anomaly tends to go away. Renaissance was first on the scene at many opportunities to take money from the markets for free. That must have helped. It's also noticeable that Simons was an academic first and foremost, who hired managers based on their mathematical ability, and avoided Wall Street groupthink by keeping his base well away from New York in Long Island. But ultimately, taking all of this into account, Simons did what he did better than anyone else. .Cliff Asness, the billionaire founder of AQR Capital Management and one of the most successful quant investors, offered his thoughts in a fascinating thread on X (formerly Twitter). The money quote, coming from a hugely successful manager in a very similar line of work to Renaissance, is: "To state the obvious, if we (or I) had a deep knowledge of how Medallion did it we'd do it too!".We will never see the likes of James Simons again. Rest in peace. .Survival Tips.Simons' story was difficult to tell, but some found a way. Katherine Burton told the history of Renaissance beautifully for Bloomberg News in 2016; and the Wall Street Journal's Greg Zuckerman produced The Man Who Solved the Market, a book that gets as close to how Simons did it as anyone is ever likely to get, in 2019. For the man himself, unfiltered, this is Simons giving a 16-minute speech about his life story to the Norwegian Academy of Science and Letters in 2022, and here he is in conversation about his investment methods at the same event. He seems far more excited by his mathematical breakthroughs than by all the money he made. And it's hard not to share in the excitement, even if the air of mystery around Medallion will likely continue. It's all worth reading. Have a good week everyone. .Read also:.Reserve Bank holds firm on interest rates despite lingering inflation concernsDaily moral struggles as Zimbabwe's inflation rate reaches 1024% – Cathy Buckle🔒 Wall Street's high-stakes, all-or-nothing bets on economy's resilience amid inflation battle.© 2024 Bloomberg L.P.